Robertet (2)

A global leader in natural fragrances, flavors and ingredients. Part 2: a virtuous business model.

How do you survive and even thrive when you are David surrounded not by one but several Goliaths? This is exactly what Robertet has done in a business where it faces much larger companies such as Givaudan, Firmenich, IFF, Symrise or its Grasse-based neighbor Mane. Robertet is “only” the number 7 player in the global flavor/fragrance/ingredients industry.

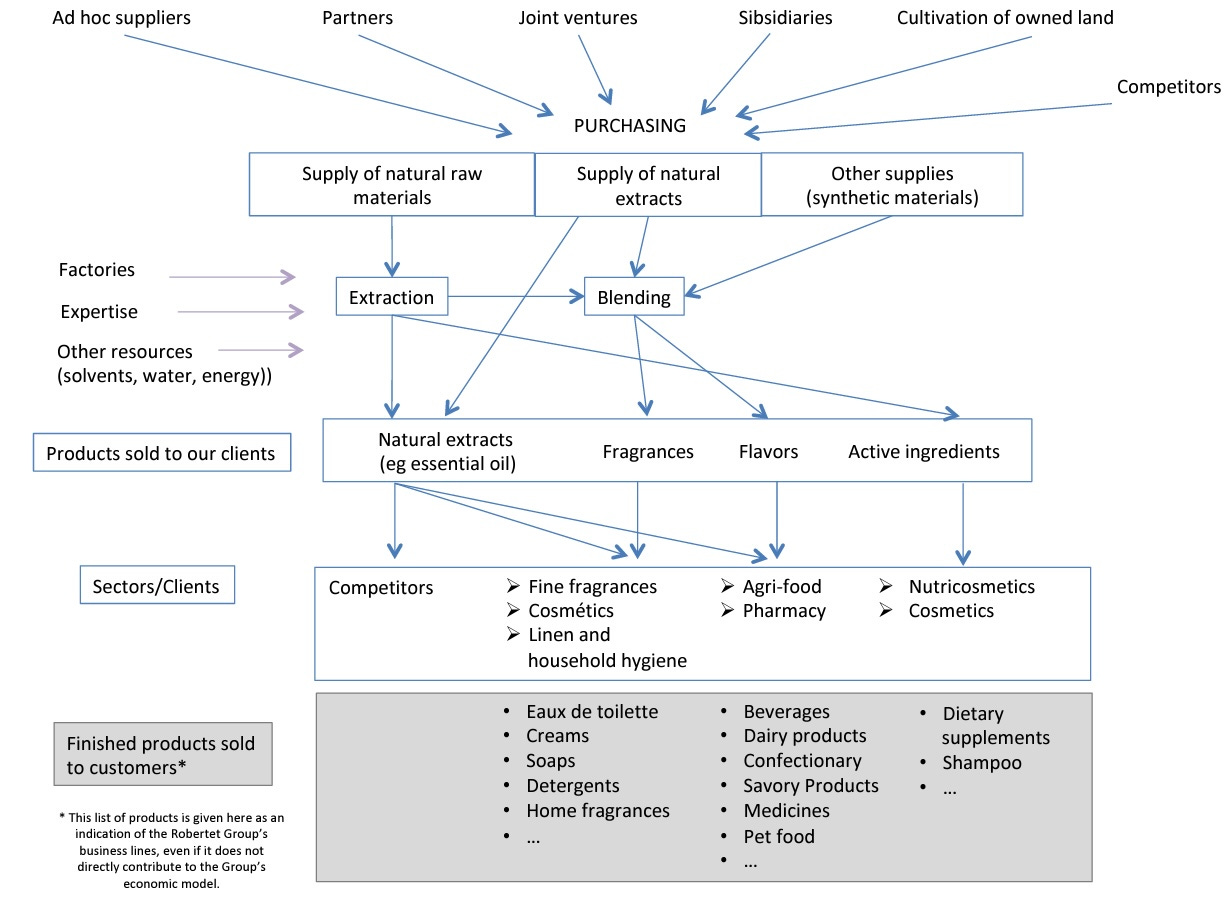

That said, Robertet does not really compete with them per se as it focuses on a smaller but more attractive niche that it has been dominating for decades: naturals. While others were favoring synthetic products, Robertet has honed and concentrated its know-how, skills and craftsmanship for 150 years to become the leading provider of naturals to the largest (but not only as it serves a diversified base of 5,886 clients) names in the perfume (Chanel, Dior, Guerlain, Burberry…) and food (Danone, Coca-Cola, P&G…) industries. Its 4 divisions now supply natural raw materials/extracts (including to some of its competitors!), fragrances, flavors and active ingredients made from 1,461 natural references sourced in 60 countries.

Robertet, over time, has built a strong moat and is now uniquely positioned to consistently deliver expected quantities of top-notch natural and critical products to extremely demanding clients. This makes switching (is it even an option?) costs extremely high for its clients and its business almost impossible to replicate from scratch by new entrants. Robertet’s main competitive advantages are:

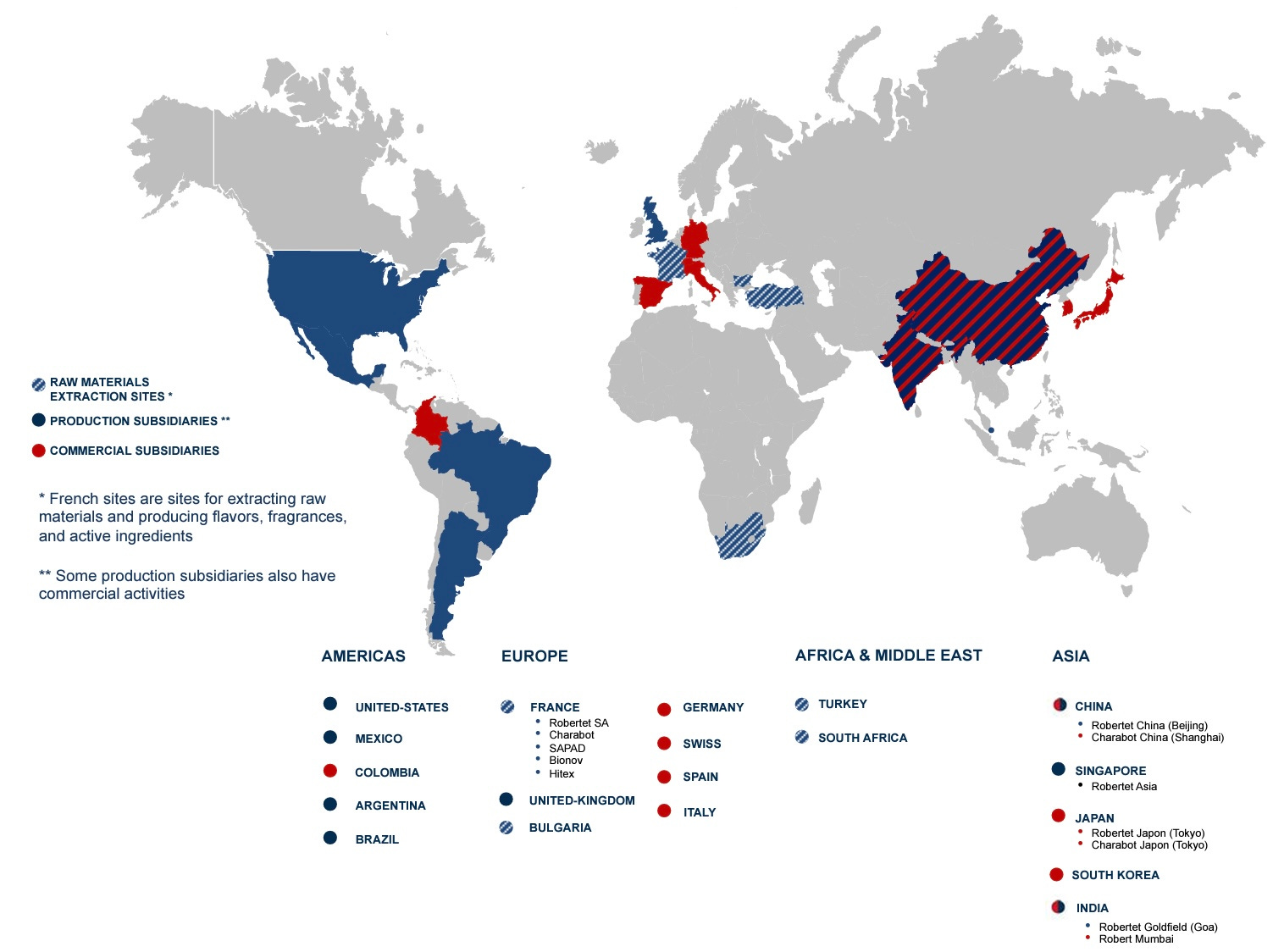

-A wide range of innovative and high quality products sold globally. The company spends between 8 and 10% of its annual revenues in R&D. Organically and through acquisitions, it has ventured into as widely diverse areas as savory aromas, beverage flavors (ice teas, flavored waters…) and, more recently, created a division dedicated to beauty and health whose potential looks very promising. Europe now represents 34% of its sales with the US and Asia-Pacific accounting for 37% and 18%, respectively.

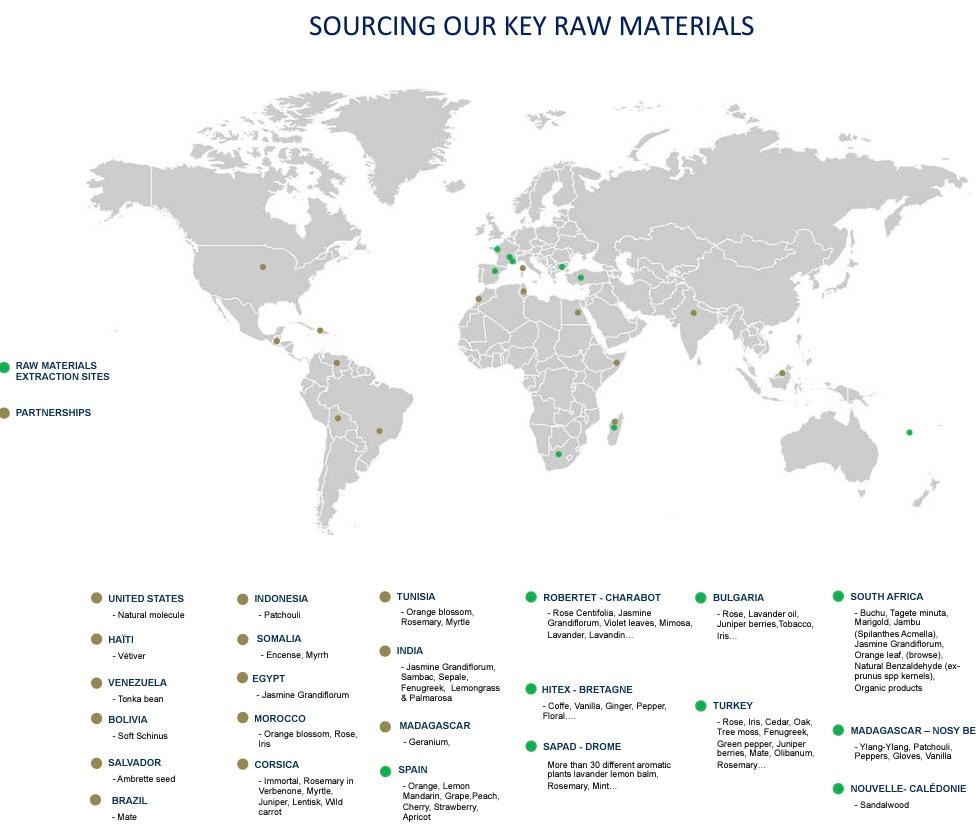

-A highly integrated value chain. The company has built 30 state-of-the-art industrial sites located as closely as possible to their sourcing regions, which has required significant CAPEX over a long period of time. 80% of its natural references volumes are now purchased and secured under long-term partnerships (above 3 years) with 67% of its 1,139 suppliers and its also farms its own land for some cultures, which overall guarantees a high degree of continuity and quality. The company has developed a clear edge in managing the logistics of such a complex supply chain.

-A long history and culture of corporate responsibility. Robertet has shown an unwavering commitment to providing traceable products to its clients with an ever growing share of organic references. It is also on a path of constant improvement to ensure its compliance with strict standards and objectives in terms of sustainability and ethics.

-Close relationships with its clients. Robertet has 14 creative centers around the world that help develop products meeting its clients’ high expectations.

Not only has this original model made Robertet a leading niche player, it is also the foundation of a high-recurrence/visibility/margin business serving growing or recession-proof industries (the food and luxury goods sectors are expected to grow at a 3-5% annualized clip over the next few years). This resilience was once again tested and demonstrated in 2020 with stable revenues (at constant exchange rates) despite an environment deeply impacted by the Covid pandemic.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in Robertet at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).