Precia Molen

A compounder that punches above its weight. Part 1: Summary thesis.

Precia Molen (ticker: PREC.PA) remains one of our favorite investment ideas and a sizable position in our respective portfolios. We also believe it is still an attractive compounding proposition at its current valuation.

This article is our summary thesis since one should be able to distill an investment rationale to a few sentences or paragraphs. In addition, you might not want to risk a reading indigestion as soon as our first post. This is a starting point and we will expand on these building blocks over the next few weeks.

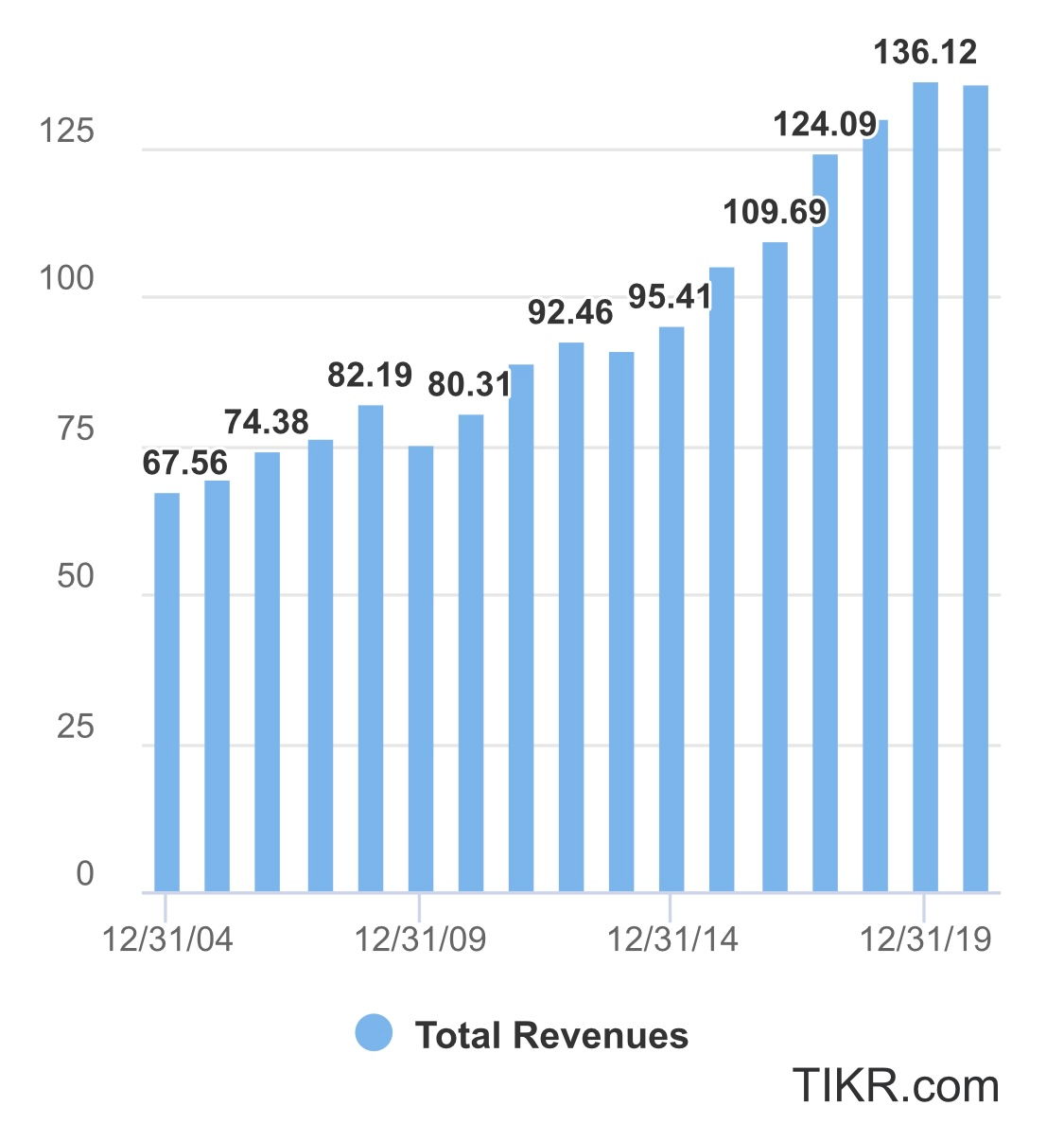

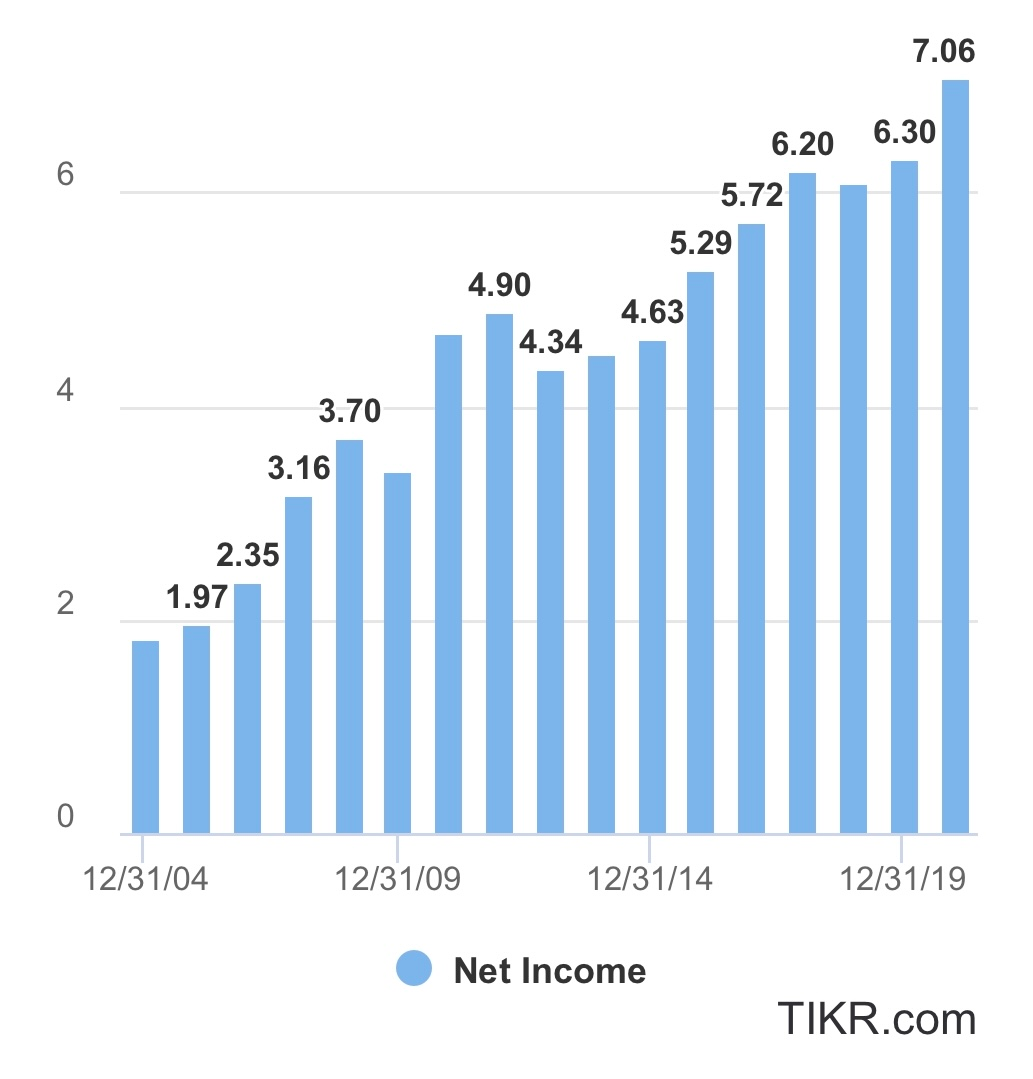

Precia was founded in 1951 and publicly listed in 1985. Its predecessor company traces its roots back to a small repair workshop established in the 19th century. Precia Molen has since become one of five top leading players in the fragmented global industrial weighing industry, with €136m in revenues and €7m in net income for the fiscal year 2020.

Its business model relies on 2 pillars: equipment sales and services, each representing ca. half of Precia’s revenues. It provides the company with both recurring revenues and higher margins, thus enhancing the visibility and predictability over its future results and cash flows.

Precia’s growth has accelerated over the last 2 decades, driven by a series of small and successfully-integrated acquisitions both in France and overseas as well as organic revenue increase. The company’s rock-solid balance sheet and a sound free cash flow generation have supplied the required resources to pull this feat off.

Its most recent foray into digitization and SaaS is extremely promising. It will hopefully be instrumental in Precia’s ongoing efforts to boost its revenues and margins further through a greater contribution of an expanded services business.

Combined with a very disciplined expense management and a savvy capital allocation, the top line growth has resulted in a net income CAGR of 9% over the last 16 years and a booming share price that skyrocketed from €22 in 2004 to €264 today (or a market capitalization of €143m).

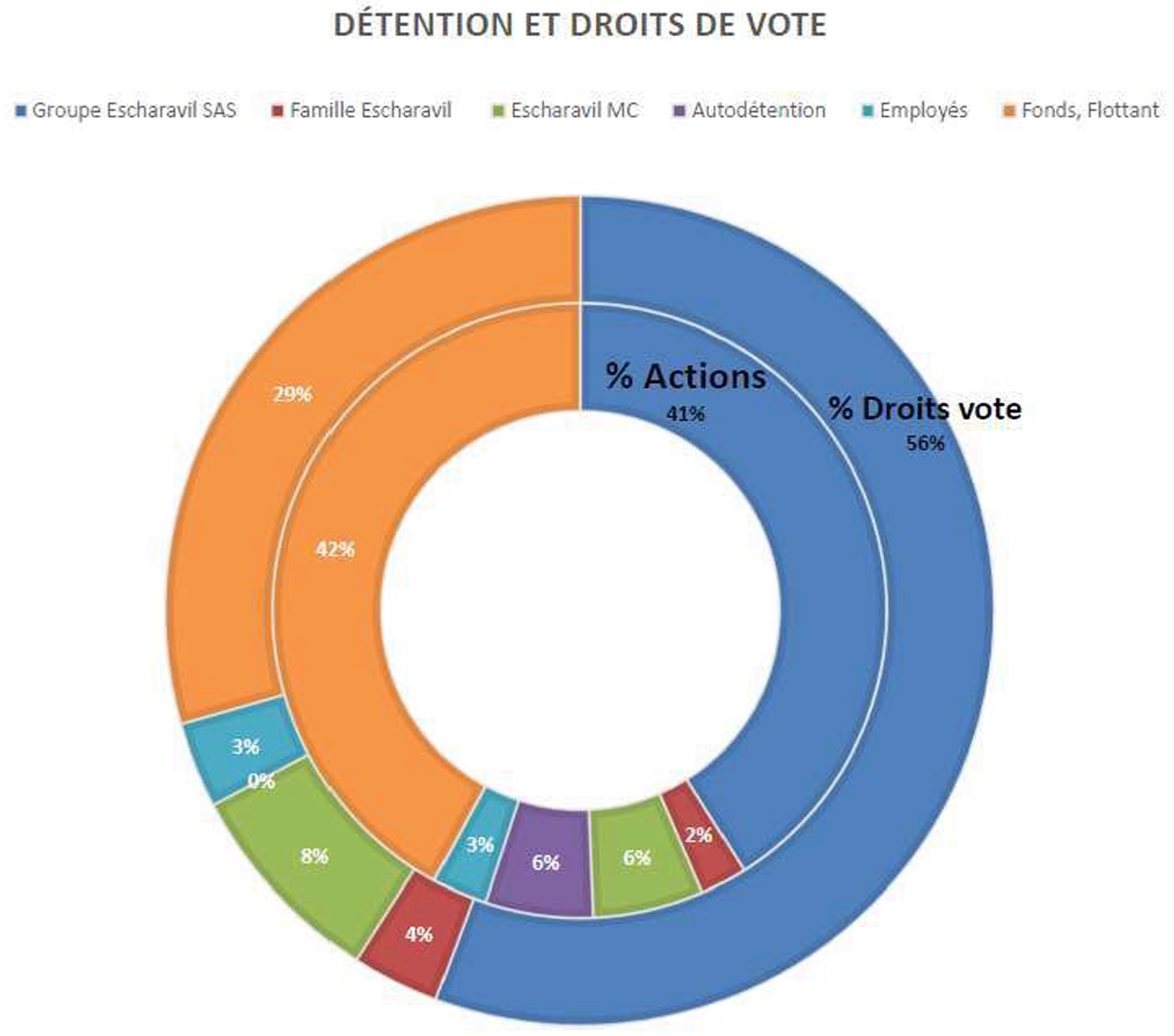

Precia shareholders also benefit from a strong alignment with both its management and founder’s heirs. The company has remained majority-held by the Escharavil family (blue/red/green in the pie chart below) for 4 generations while employees and management also own a smaller portion of its shares via an ESOP.

Precia’s valuation remains reasonable, especially for a company consistently reinvesting 80%+ of its profits at a fairly stable 11% ROE (13% ROIC given the structural net cash position), while also enjoying a long demonstrable track record of growth. Based on the company’s most recent guidance and current share price, we expect a free cash flow/owner earnings yield of approximately 8% and an EV/EBITDA ratio of ca. 6 for FY 2021. Factoring in even some limited organic LT growth, Precia shareholders might well be in a position to achieve a double-digit return over the long-run without sacrificing their margin of safety.

We hope this already gives you a good sense of the company and whether you want to continue to explore our thesis in more details over the next few weeks.

Next time, we will share more on Precia’s history, business model and strategy. In the meantime, thanks again for signing up and feel free to talk to your friends / fellow investors about our Substack. You can also reach out by email or by DM on Twitter @FRValue @FoxCastlehold. Have a great week ahead.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in Precia Molen at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

Looks promising. Incredible how cheap the stock was in the early 2010s