Precia (4)

A compounder that punches above its weight. Part 4: Capital allocation and valuation.

Precia has historically used all the following capital allocation levers at its disposal to put its free cash flow to work while maintaining a positive net cash position on its balance sheet: dividends, acquisitions, share buybacks and reinvestment in its existing operations.

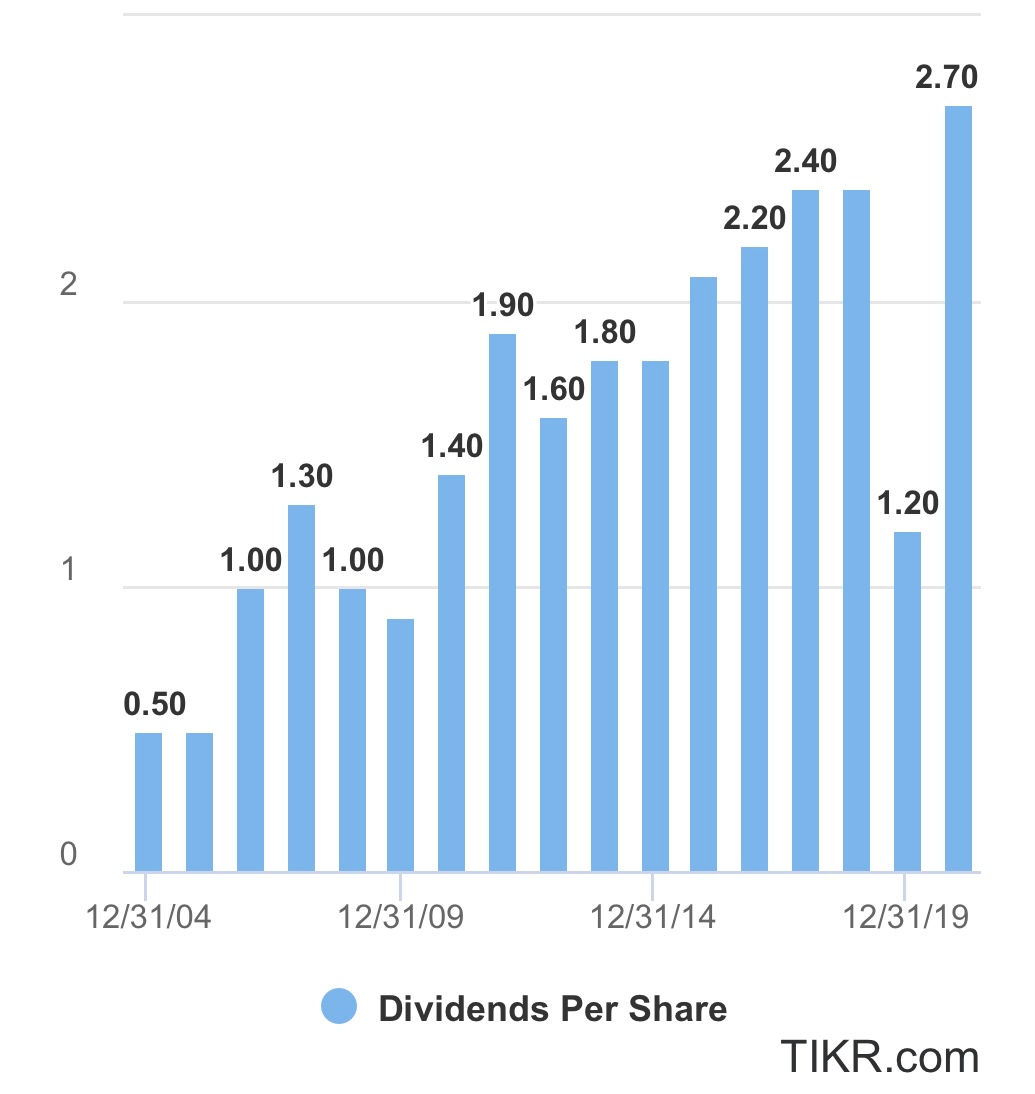

Precia’s dividend policy has been quite conservative over the past 16 years with a payout ratio hovering around 20% and an average yield of ca. 1% since 2015. In keeping with its profits, its dividend per share has increased at a 11% CAGR over the 2004-2020 period to reach €2.7 today.

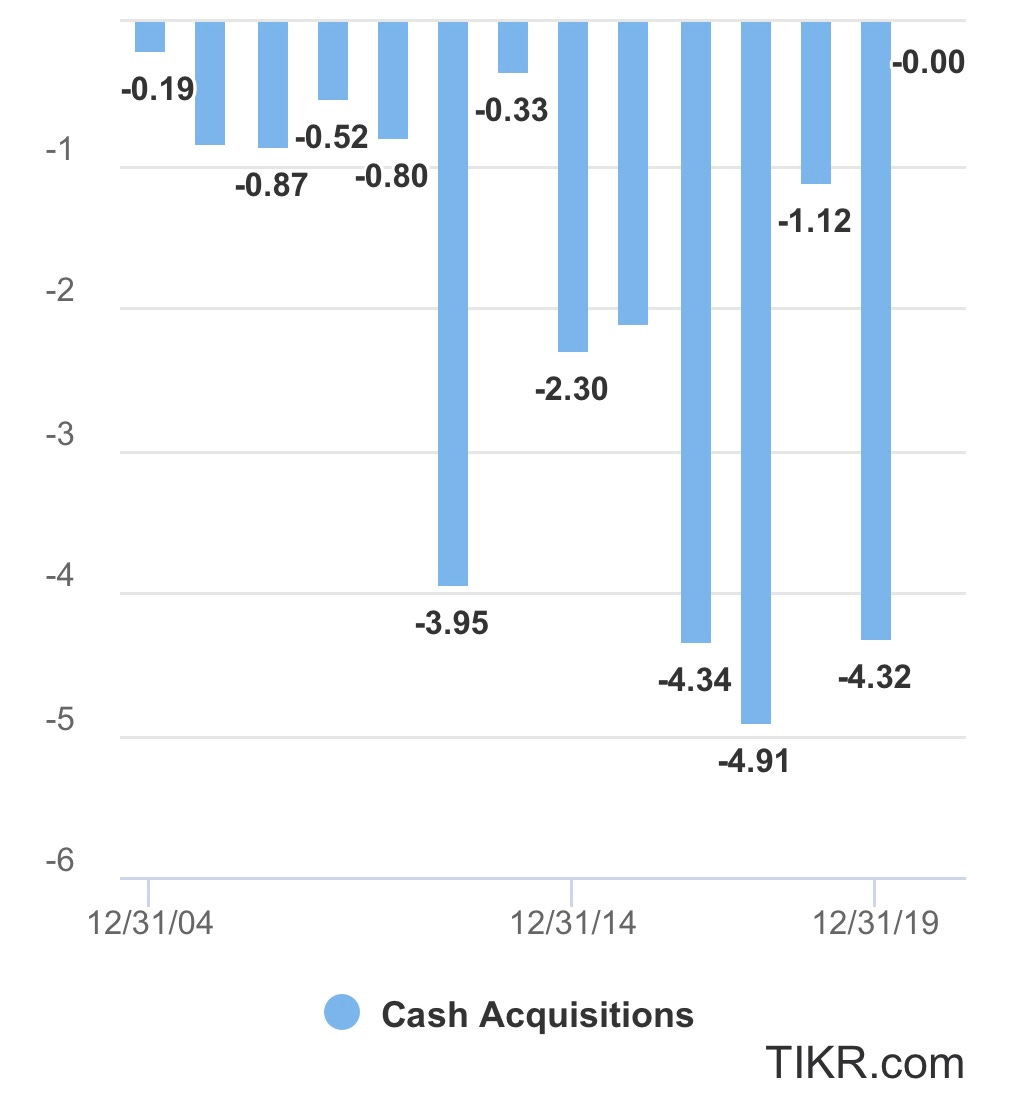

Precia’s main focus has however been on acquisitions and it has spent up to €4m-5m p.a. since 2016 while remaining very disciplined on multiples paid (usually no more than 6x EBIT). As mentioned in our previous article, the bulk of it was used to improve its network coverage mainly in France (Epona, JAC Pesage…), Australia/New Zealand (Adelaide Weighing and Weighpack), Africa (CAPI) and Eastern Europe (Milviteka) with spectacular ROIs so far in the last 2 cases.

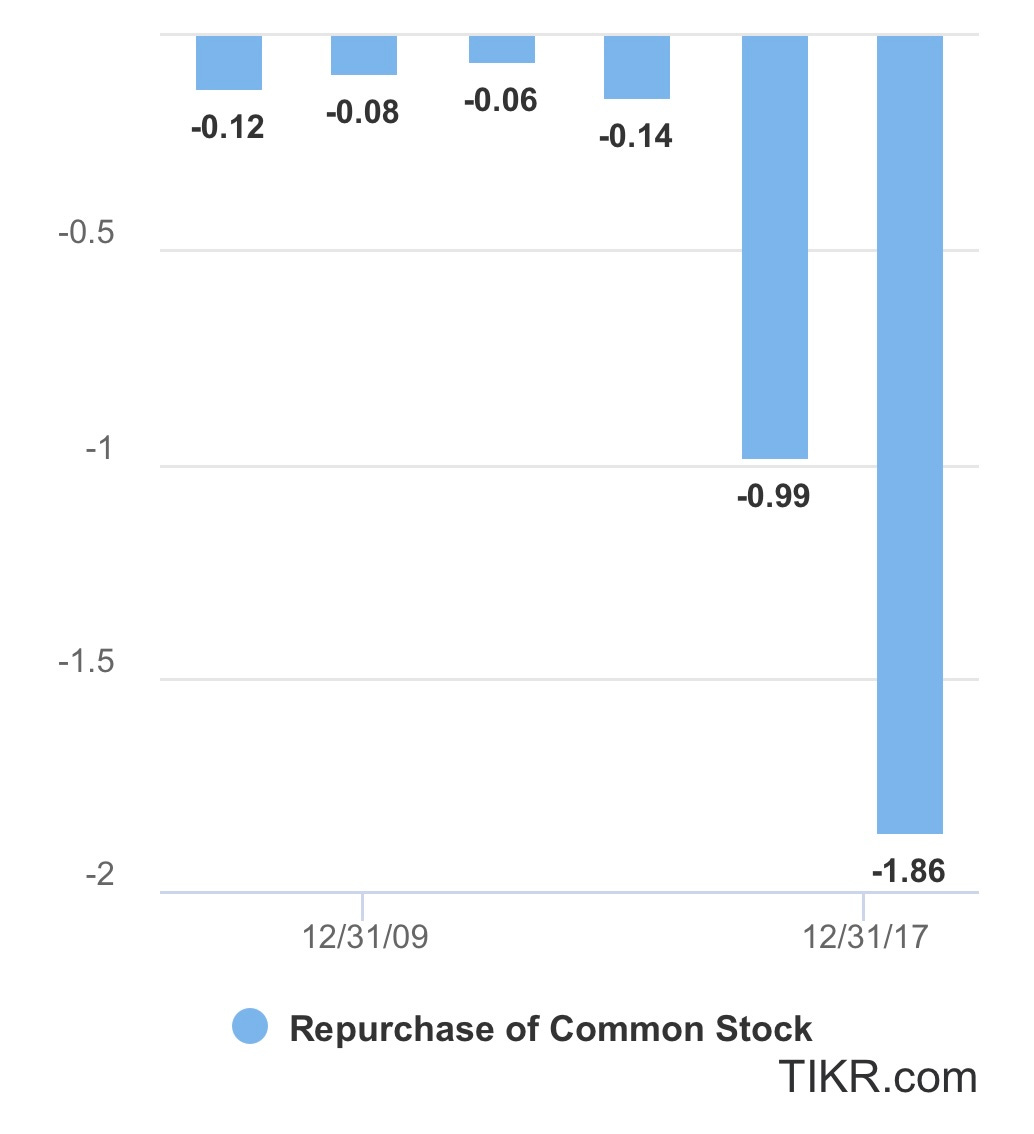

Its stance in terms of share repurchase has been more opportunistic but overall savvy. Its most recent buybacks occurred in 2018 for a combined €1.9m at a max. share price of €196. It now sits on 32,663 treasury shares bought at an average €97 and representing a €5.7m in latent capital gains based on today’s share price (€272).

Although not as cheap / as much of a bargain as last year (when we built the lion’s share of our own position), we believe Precia’s valuation is still reasonable at the current share price. Based on our projections, Precia’s owner’s earnings (net income plus amort./deprec. minus maintenance capex) could well end up in a €9-10m range in 2021 vs. ca. €8m in 2020. This would result in an ex-cash earnings yield of 7-8%. Given Precia’s historical earnings growth of 9% since 2004, consistent with its 80% reinvestment rate at a 10+% ROE/ROIC, the overall return for the long-term investor building a position at today’s price could still remain in double-digit territory.

Taking a “private-market” valuation approach would lead to a similar conclusion as Precia could command an EV/EBITDA of 6-7 based on our expectations for its FY21 results. This is well below the current average multiples paid for private or public companies in Europe, as shown below.

That said, it might be somewhat more prudent or sensible to buy shares at a maximum price of €265, which is the upper limit of the company’s share repurchase program that should be approved by shareholders during this week’s AGM.

This pretty much wraps up our initial series of articles on Precia. Thanks again for signing up and feel free to talk to your friends / fellow investors about our Substack. You can also reach out by email or by DM on Twitter @FRValue @FoxCastlehold. Have a great week ahead.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in Precia Molen at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).