Precia (3)

A compounder that punches above its weight. Part 3: Recent operating performance and M&A transactions.

Precia’s recent operating performance has demonstrated the company’s resilience in the face of an unprecedented crisis.

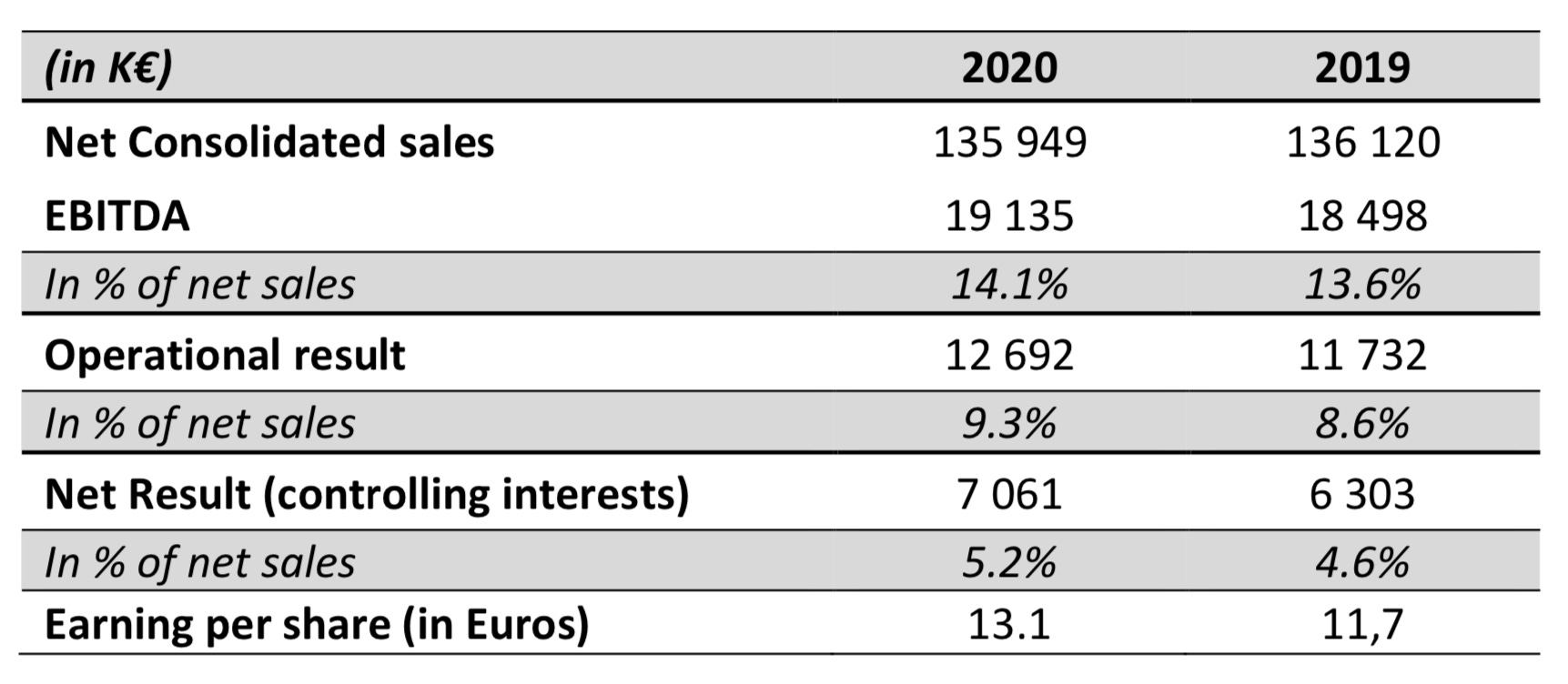

In a very challenging environment created by the COVID-19 pandemic, Precia managed to keep its 2020 revenues at €136m, a level similar to 2019. This was achieved through the incremental contribution of Milviteka (acquired in 2019, see below), a strong recurring revenue base and despite a negative 5% organic decline.

Precia’s EBIT improved from €11.7m to €12.7m thanks to Milviteka’s solid operating performance/higher margins and a stringent expense management. Net income was up ca. 13% at €7.1m with a FCF generation of €6.1m (after IFRS16 leases impact of €3.1m). The company’s net cash position soared to €15.1m (excl. IFRS16 debt of €8.8m).

Precia maintained its strong H2 ‘20 momentum during the first quarter of 2021 and generated revenues of €35.4m, up 18.9% (20% organically) vs. the same period last year. The backlog is above where it was pre-Covid and all geographies posted significant increases. Precia projects its revenues should climb to €140-145m for FY 2021 with a growing EBIT.

Raw material shortages and price inflation represent a potential downside risk though. We believe it is mitigated by Precia’s pricing power potential due to the mission critical nature of its equipments/services as well as its dominant position in some markets / industries.

The subsidiaries’ contribution to profitability still remains fairly concentrated amongst a few very successful operations.

After PMS, the French services business that accounts for ca. 60% of its net income, Precia’s Indian operations remain the crown jewel of its foreign subsidiaries. Due to its high-end positioning and low-cost onshore operations, this subsidiary enjoys a 20% net margin and posted a FY’20 net income of €1.1mm in a very difficult operating context where revenues declined 25%. Following the opening of a second factory in May 2021, manufacturing capacity should double and allow Precia to take full advantage of this market’s opportunities.

Milviteka (see more details below), Molen (Netherlands) and the African operations (CAPI and Morocco) are also star performers with respective contributions to Precia’s consolidated bottom line of €1.1m, €0.8m and €0.6m on 2020.

Some subsidiaries remain loss-making either due to a lack of scale (Australia, Brazil) or a disappointing integration (UK). Their turnaround is ongoing and managements changes have been recently done (Australia, UK) or sizable contracts won (Brazil).

Two small and highly profitable acquisitions could prove transformative going forward.

Milviteka, based in Lithuania, was acquired by Precia for ca. €4m in 2019. It is active in designing and manufacturing bulk / grain handling (incl. dosing and weighing), processing and storage systems. It adds more higher-margin solutions to Precia’s already strong product line-up towards the bulk/agri industries, which it will be in a position to offer to existing and new clients globally.

Precia will benefit from a better access to bulk terminals, CEE markets such as Russia and Ukraine as well as cost-efficient manufacturing capabilities with no foreign exchange risk (Lithuania being a Euro-area country). With revenues of €7.6m for a net income of €1.1m, Milviteka’s contribution to Precia’s 2020 results was already significant and the acquisition price looks like a bargain at this stage.

In May 2021, Precia closed on the acquisition of a 80% stake in the MES software publisher and Lyon-based Creative IT for ca. €4m. The remaining 20% shares will be owned by a group of managers.

MES softwares facilitate the collection, analysis and monitoring of industrial data in order to streamline industrial processes. They are a critical layer of IIOT (Industrial Internet of Things) systems and are instrumental to deliver on the promises of Industry 4.0 in terms of enhanced traceability/quality, reduced waste/downtime, customization and overall equipment effectiveness.

Source: Visschers-Consulting

Creative IT, through its Qubes solution, generated €3.2m in 2020 revenues. It boasts an installed base of 209 clients on 500 industrial sites globally, high profitability (EBITDA margin of 25%) and projected top line growth (15% p.a. over the next 4 years) as well as sizable recurring revenues (80% of total sales). It will boost Precia’s data/digital offering while also giving it access to the fast-growing MES market and further increasing the importance of its services business.

Overall, Milviteka and Creative IT solutions diversify Precia’s existing portfolio with a complementary stream of high-margin businesses. They will thus help capture a larger share of its clients’ critical equipment/services spending. Finally, they could represent up to 20-25% of Precia’s net profits going forward.

Next time, we will wrap up this series of articles on Precia by covering its capital allocation and valuation. In the meantime, thanks again for signing up and feel free to talk to your friends / fellow investors about our Substack. You can also reach out by email or by DM on Twitter @FRValue @FoxCastlehold. Have a great week ahead.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in Precia Molen at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).