IGE+XAO (1)

A special situation in the French software industry

IGE+XAO is the French leading player for electrical CAD (Computer-Aided Design)/PLM (Product Lifecycle Management) softwares, used in the design and maintenance of electrical installations, with a domestic market share of close to 70%. Over the past three decades, IGE has also expanded in Europe and beyond but remains a more marginal player overseas despite partnerships with Dassault Systèmes, Siemens, … It serves a wide variety of industries (aerospace, automotive, construction, …) and clients of various sizes (incl. the likes of Renault, Airbus, …).

Due to high switching costs and the dominance of its niche in France, the company commands high operating margins (in excess of 30%), a ROE/ROIC of ca. 20% and a history of high FCF generation resulting in a significant net cash position of €53m.

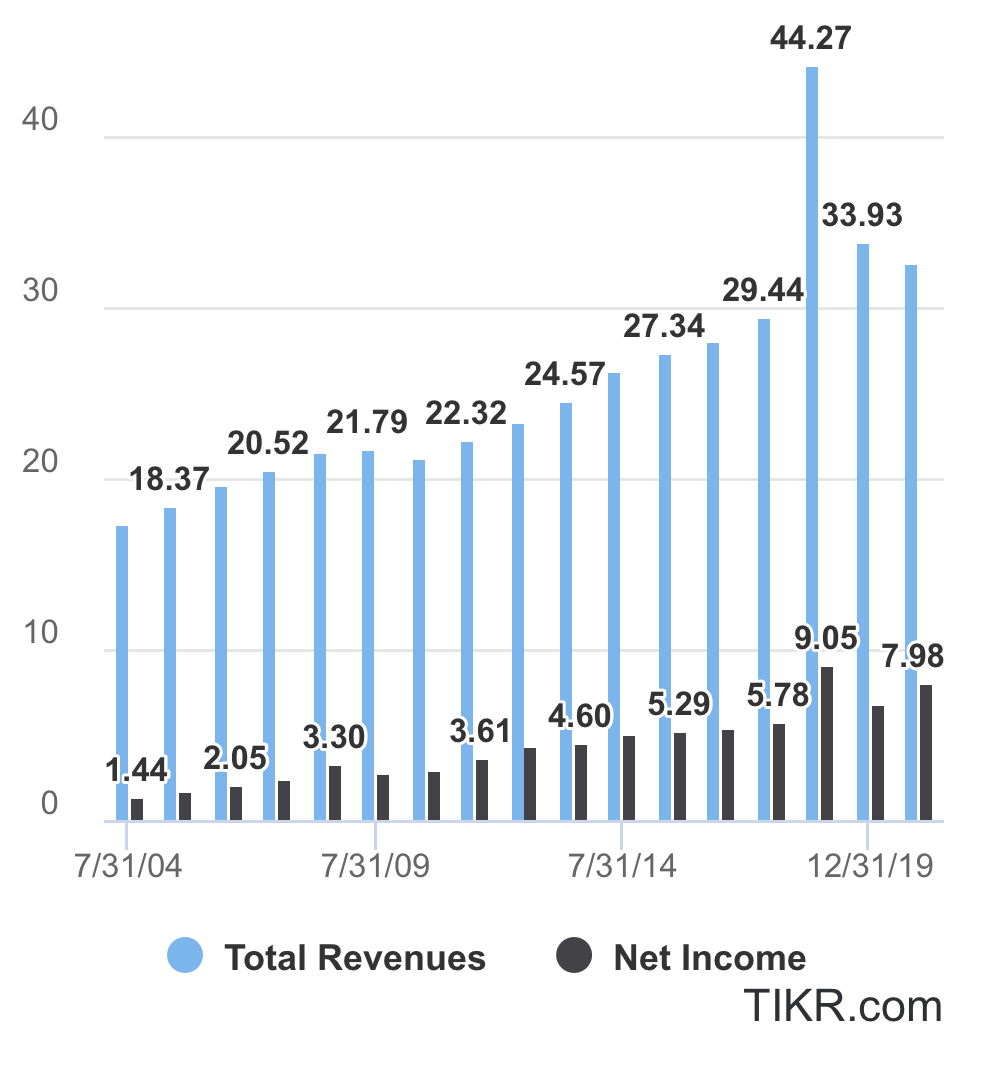

Driven by revenue and net income CAGR of 5% and 11%, respectively, from 2004 to 2019, IGE’s share price has increased more than 30-fold since its IPO in 1997, also supported by a savvy and opportunistic buyback policy.

Schneider Electric offered €132 per share in 2018 to take over IGE but failed to squeeze out minority shareholders and ended up with only 67.7% of its shares and 78.3% of voting rights, as of today. It is now trying again with a bid of €260 per share (or a 15% premium over the last pre-offer share price) to acquire the shares it does not own yet.

Multiples for the proposed transaction (EV/revenues of 9x and EV/EBITDA of 26x) are largely in line with those of recent larger multi-billion dollar acquisitions made by Schneider or its subsidiary Aveva in the software space (RIB Software and OSIsoft), despite being somewhat below those of (faster-growing) French SaaS listed comparables such as Sidetrade or Esker. One could further argue that IGE’s growth potential (especially overseas through synergies with Schneider) and increased recurring revenues (ca. 55% currently) following its ongoing transition to SaaS should call for an even higher consideration.

That said, such a debate over valuation, although intellectually satisfying, seems to be somewhat moot at this stage as two of IGE’s largest minority shareholders, Gay-Lussac Gestion and Orfim (with a current combined ownership of 10.5%), have publicly declared they would not tender their shares at the proposed price (we suspect other fund managers might follow suit…). Orfim has even increased its stake from ca. 5.3% to 7% during the past week.

So what’s next for IGE’s shareholders? There are a few possible alternatives. 1) Schneider could sweeten the existing offer. We believe this is likely as they might want to put behind them an already protracted take-over process. 2) Schneider could proceed with the existing offer but it will eventually end up with less than 90% of the shares and voting rights required to trigger a squeeze-out. IGE would thus remain listed and €260 would likely act as a new floor for the share price (as the previous offer price did for the last 3 years). 3) Schneider could withdraw its offer entirely. We do not really believe in this scenario as Schneider clearly wants to take full control of IGE.

In any event, as existing shareholders of IGE, we purchased the bulk of our shares in 2020 at a FCF yield close to 10% (vs. 4% now) and will not tender them as long as we are not forced to. We strongly believe there is no real downside in doing so and IGE can still grow its profits/FCF at a min. 4-5% annualized clip and compound value nicely over the long run. Today’s share price of €262 seems to indicate the market agrees with such an approach…for the time being.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in IGE+XAO at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).