Gérard Perrier Industrie (1)

Gérard Perrier Industrie (1)

Part 1: Introduction and company overview

« Our company will last longer than those who created it and those who are part of it today ». Gérard Perrier, founder of GPI.

We usually do not pay much attention to companies’ mottos per se. We like owners who do what they say and say what they do. But in the case of Gérard Perrier Industrie (GPI), the above quote / mission statement perfectly summarizes more than anything else what the company and its owners have been achieving over the past 5 decades: building a great, enduring and resilient business for the long-run.

Source: GPI

Founded in 1967 by Gérard Perrier in Belley (~85kms East of Lyon), the eponymous group consisted initially of SOTEB, still specializing in the installation and maintenance of large industrial sites. In 1970, a new subsidiary, Geral, was added. It now designs and manufactures a wide array of custom-made electrical and electronic equipments incorporated in its clients’ machinery or processes.

Since its establishment, the group has further expanded into multiple spaces including automation, instrumentation, IT and software while also penetrating more industries, regions and niches. It has thus become a French leading independent supplier of industrial electrical solutions serving an ample roster of large multinational clients such as EDF, Arcelor, Total, Arkema, Sanofi, Siemens, Schneider Electric, Airbus, Safran, General Electric and many more.

Source: GPI

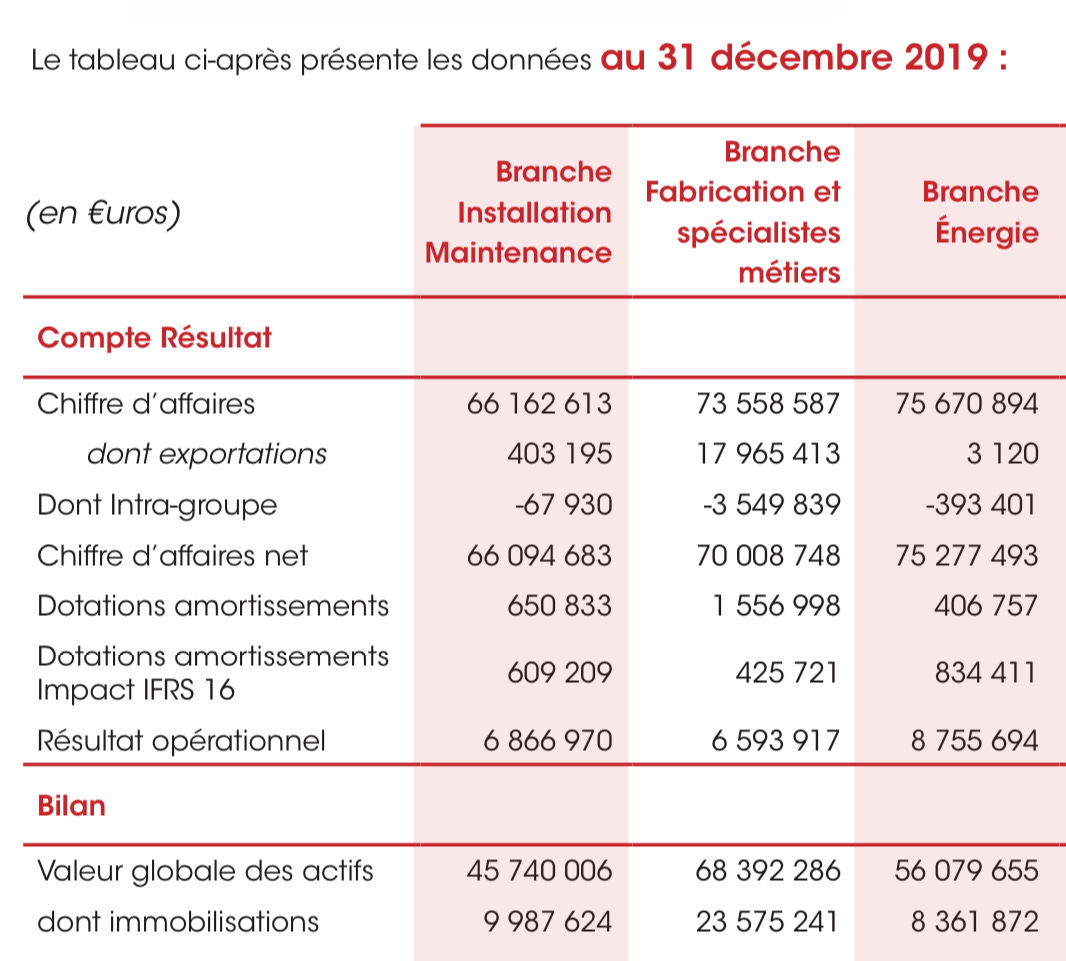

In 2020, despite a difficult context, GPI generated €191m in revenues (vs. €211m in 2019), with each of its 3 divisions (installation/maintenance, manufacturing and energy services) contributing rather evenly. Thanks in part (but not only as we will explore in more detail in the second article) to an asset-light business model and multi-year contracts in its 2 installation/maintenance divisions, it also boasts solid operating margins (8.2% in 2020 vs. 9.6% in 2019), superior returns on invested capital (close to 20% in ‘17, ‘18 and ‘19) and highly recurring revenues (for ca. 2/3 of its combined sales).

Revenues/Op. Income and Asset breakdown across GPI’s 3 operating divisions in 2019 (a “normal” year). Ex-holdco. Source: GPI annual report.

Over the past 16 years, GPI has grown its revenues and net income 8% p.a. organically and through a combination of well-targeted acquisitions. GPI has been using its free cash flow (ca. €10m in 2020 vs. €14m in 2019) very intelligently using the full spectrum of the capital allocation toolbox not only to make acquisitions but also to pay dividends and repurchase shares while also building a sizable cash war chest. Its savvy usage of both the stock market and private equity (PE), through a series of OBO (Owner’s Buy-Out), to strengthen the family ownership, group independence and fund its growth also stands out.

As a result of this outstanding operating performance, combined to the stock’s multiple expansion, the share price has increased 175-fold from its low of €0.48 in Jan. 1994 to €84 today (i.e. a 21% CAGR over 27+ years, ex-dividend). GPI now has a market capitalization of €304m, employs 1,758 people across 14 subsidiaries and is 52%-controlled by the Perrier family through its 73%-owned holdco, Amperra.

Share Price History - Source: Morningstar

At a FCF yield of ca. 6% and an ex-cash PE of 18x, based on our expectations for FY 2021, the valuation is clearly not cheap (unlike the bargain it represented, in hindsight, in 2020). That said, it also reflects the quality, visibility, resilience and recurrence provided by GPI’s business model as well as attractive growth prospects, hopefully on par with the last 16 years, driven largely by opportunities in new markets whether in terms of geographies (in France and abroad) or products (industrial internet of things, industry 4.0, ...).

Over the next few weeks, we will delve deeper into GPI’s business model, the values and approach underpinning its achievements. We will also cover its successful history of acquisitions, capital allocation, use of PE/OBO, valuation and more recent events.

Disclaimer: The above article constitutes the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. Disclosure – we hold a position in Gérard Perrier Industrie at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

Congrats on digging up this little gem! Truly outstanding results.